EV Slump?

February 27, 2026

Alex KiersteinEV registrations fall off in the latest data, which captures the tax credit repeal. But maybe it’s not as gloomy as it could have been.

The things you would expect to happen in 2025 with new EV sales did. (Or, at least, with EV registrations, which is how S&P gets around a limited amount of car sales data from companies like Tesla.) The repeal of the federal EV tax credit caused a surge in registrations, and then a steep drop off. But the whole-year decline, despite all that drama, is modest. And my theory is that the EV market moving forward will be driven almost entirely by one factor: price.

Automotive News has a pretty good summary of the most recent S&P Global Mobility registration data. The bottom line is that EV registrations declined by 0.4% in 2025 compared to the year prior. Remember, the tax credit went away on September 30, so there was a rush to capitalize on it and then a slump afterward. AN notes that EV market share stabilized somewhat overall. In 2023, it was around 10%. By November, that had slumped to 4.6%.

Automakers have responded in a variety of ways. Obviously there’s the broader reordering of the market, with many automakers retreating from EV offerings and pouring resources into hybrids. There are some unusual outliers, like the slew of offerings from Toyota (Highlander, C-HR, a refreshed bZ) and Subaru (a refreshed Solterra and the new Trailseeker and Uncharted models).

Many automakers are also offering cash incentives to reduce the cost of entry, helping to erode one big EV weakness. EVs still cost more than an “equivalent” gas or hybrid vehicle, although equivalence is going to be subjective due to the many points of differentiation. Battery pack prices are a significant cost, even as the cost-per-kWh falls.

Using Bloomberg’s numbers, let’s say a 2026 Subaru Solterra’s 74.7-kWh battery was built in the US for the average $120/kWh local production price. That makes the unit, without factoring in any other costs, $9,035. Factor in the cost of the e-motors, and just the drivetrain is quite expensive.

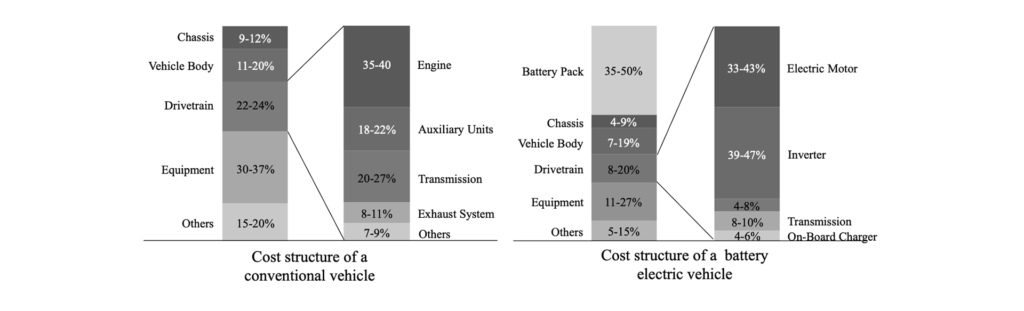

Another way to look at it is in terms of percentage of the total cost of the vehicle, and for this I have to rely on studies that make broad generalizations and assumptions and are thus really only good for, well, generalizations. This UC Davis study found that the battery makes up as much as 50% of the total cost to produce the vehicle, whereas a conventional internal-combustion powertrain is roughly 25% of the total cost.

Batteries have the unenviable task of competing with the energy density of liquid hydrocarbons while accommodating consumer desire for feature-laden, large vehicles. At the moment, it’s a recipe for weight and cost. Without the federal tax incentives, that disparity is more apparent.

And all of the up-front costs really downplay the fact that the playing field isn’t level. The fossil fuel industry receives billions in subsidies, and CAFE standards (which were just weakened, of course) don’t have much of an effect on highly profitable (and less efficient) trucks and SUVs.

It’s also hard for humans psychologically to compare a future benefit to a current cost. EVs are more expensive up front but offer the potential for significant future savings in fuel costs and maintenance—in most states, and in a home-charging scenario. Local energy costs, and public charging costs, do alter the math. All of that makes doing the mental calculus about the actual ownership costs of an EV tricky. Let’s not even start with trying to game out what EV depreciation will look like in this post-tax-credit universe.

With all that said, the registration decline last year doesn’t seem like an existential crisis for EVs. The December numbers are grim, but they don’t tell us much about long-term trends, especially after the pre-repeal surge. It seems to demonstrate a persistent level of interest in these vehicles.

It’s what comes next that will set the market. Automakers are adjusting their mixes; Ford has backed off of EV offerings in the short-term in favor of its low-cost UEV platform which is a few years away, Nissan has delayed its lower-cost Leaf variant, and Honda seems likely to bail on the segment altogether. For those automakers hoping to stick it out, will they attack cost or try to recoup investments by prioritizing only the most profitable EVs?

I don’t think automakers can address the cost-of-entry issue without economies of scale, and they will need to emulate or license the latest battery tech (pioneered by Chinese firms) to compete. That is a bet that entails significant costs, and even with the tariff uncertainty, likely more investment in US production, with all of the labor cost issues that entails. (And, to be fair, the local subsidies that seem to be de rigeur for any American manufacturing facility.) And I don’t think they can grow EV market share without attacking cost-of-entry.

I think this is what Toyota is exploring. Decisions made years ago, in a different EV environment, influence the products we see today. But 5% of the total car market is a significant chunk. I predict that if Toyota’s latest EVs do well, and if Subaru can see some sales growth off the back of its SUV trio, others may keep their EVs in the market to compete. 2026 is going to be a very illustrative year for EV market trends.

Recent Posts

All Posts

February 26, 2026

February 25, 2026

February 24, 2026

Leave a Reply